Top Real Estate Agents: Best Realtors for Gated Communities in Palm Beach County

Although our focus is on commercial real estate, we though this post would be of interest due to the volume and value of sales; $6.1 billion in gated sales last year.

Palm Beach County’s gated enclaves feel like private resorts—guard posts, leafy boulevards, and five-star clubhouses. Yet every community enforces its own fees, pet limits, and even paint colors, so the agent you pick determines whether you breeze through the gate or idle at the kiosk.

Demand is scorching: the county’s 25 busiest Realtors closed $6.1 billion in gated sales last year, with one broker alone logging $636 million inside a single neighborhood, according to a March 2025 Real Deal ranking.

The market is vibrant, the rules are tricky, and you need a specialist who speaks fluent HOA. The seven pros below do exactly that—handing you the keys with confidence.

Quick-scan: which agent fits your gate?

We promised you specialists, not a phone-book pile of business cards. Before we dive into full profiles, here’s a rapid look at who works where and why that matters.

Each name below links to thousands of gated-community closings; one record even crosses the nine-figure mark. We trimmed the noise to five datapoints you actually care about: focus, experience, sales, reputation, and proof.

| Realtor / team | Gated-community specialty | Years in niche | 2021–2024 gated sales | Average review score |

| SquareFoot Homes (county-wide) | Family and luxury communities from Arden to Boca Bridges | 10+ (team) | about 50 closings across multiple neighborhoods | 4.9★ |

| David W. Roberts (Boca Raton) | Ultra-luxury Royal Palm Yacht & Country Club only | 40+ | $636 million in 2024 | 5.0★ |

| Eric Telchin Group (West Palm) | Ibis Golf & Country Club plus other 33412 golf communities | 15 | 200+ deals; more than 1,000 career sales in Ibis | 5.0★ |

| Jeffrey Katz Group (Boynton) | 55-plus Valencia active-adult communities | 20 | over $325 million sold | 5.0★ |

| Tricoli Team (KW) | Mid-market family HOAs county-wide | 20 | 300+ transactions | 5.0★ |

| Alex & Margot Platt (Compass) | New-build luxury (Lotus, Bridges) | 8 | 60+ high-end sales | 5.0★ |

| Martha Jolicoeur (Elliman) | Wellington equestrian estates | 15 | 80+ barn-ready estates | 5.0★ |

Browse the grid, match an agent to your lifestyle, and read on to see how each professional clears hurdles that keep average agents parked at the gate.

1. SquareFoot Homes Real Estate Group – your county-wide gatekeepers

SquareFoot Homes Real Estate Group website screenshot

1. SquareFoot Homes Real Estate Group – your county-wide gatekeepers

Picture a concierge desk that stretches from Boca Raton to Jupiter. That is SquareFoot Homes. The boutique team lives inside the communities they sell, with one agent in Boca Bridges and another in Arden, so they trade first-hand intel rather than recycled market reports.

Because they serve the whole county, they spot trends others miss: HOAs that quietly raised security dues last quarter, golf clubs cutting initiation fees, and neighborhoods where resale values surge after a clubhouse refresh. They feed that insight into a tech-smart portal that filters listings by lifestyle—golf, 55-plus, waterfront—and flags fee changes overnight.

Reach never dilutes results. The team closed about fifty gated transactions in the past three years, ranging from starter HOAs to eight-figure estates. Repeat clients echo the same praise: “They made three sales feel like one smooth ride.” If you want choices across the map without juggling multiple agents, start here.

2. David W. Roberts – King of Royal Palm

Step inside Royal Palm Yacht and Country Club and one name echoes louder than the hum of golf carts: David W. Roberts. He has walked these streets for more than forty years, first as a resident, then as the broker who reset local record prices.

Royal Palm Properties and David W. Roberts website screenshot

In 2024 alone he guided $636 million in on-market sales, every dollar inside this single guard-gated enclave. Clients say Roberts can quote lot elevations from memory; appraisers call him for comparable data. That mastery pays off. When a teardown sold for thirty-six million, he handled both sides and defended value no spreadsheet could capture.

Royal Palm follows bespoke rules—equity memberships, marina-slip lotteries, architectural reviews with surgical precision. Roberts knows every key holder and the nuance of each bylaw. Hire him and you tap a resident network that secures permits, tee times, and seawall inspections before most agents print brochures.

If your target is Boca’s most exclusive gate, skip the learning curve. Roberts already wrote the syllabus.

3. Eric Telchin Group – the Ibis insider

Drive through the gates of Ibis Golf and Country Club and odds are the listing you pass belongs to Eric Telchin. His signs may be common as palmettos, but his method is all precision. Telchin has logged more than 1,000 Ibis closings, a record built on meticulous data and neighborly follow-through.

He tracks every sale, price shift, and membership tweak in a private spreadsheet that dwarfs the MLS. Sellers lean on those numbers to capture extra value from upgraded kitchens; buyers use them to time offers around seasonal inventory bumps. That focus placed his team third in the county for transaction sides last year while keeping a perfect five-star rating intact.

Living inside the 33412 ZIP keeps Telchin ahead of rule changes. He knows which sub-HOA will repave roads or raise capital contributions and hands clients a cheat sheet before each tour, saving them from fee surprises. After closing, he is first to invite newcomers for a quick nine or a Friday clubhouse buffet. Service continues long after the ink dries, which is why families return when it is time to upsize or downsize inside the gates.

Shopping for a golf-centric lifestyle north of West Palm? Telchin already has the tee sheet ready.

4. Jeffrey Katz Group – the 55-plus matchmakers

Active-adult buyers want more than square footage. They want pickleball leagues, grand-kid rules, and an HOA that trims hedges while they travel. Jeffrey Katz has turned those wishes into more than $325 million in closed sales across the Valencia series and other 55-plus enclaves.

His website feels like a retirement concierge desk: side-by-side fee charts, amenity videos, and comparison grids of pet policies. New clients arrive having streamed every walkthrough, then rely on Katz to decode the fine print. He guides them through age-restriction affidavits, clubhouse equity options, and the lesser-known rule that some HOAs limit overnight guests under eighteen.

Patience is his edge. Reviews read like thank-you notes—snowbirds grateful for sunrise webcam screenshots, widowers thankful for lenders who understand fixed-income underwriting. Because Katz tracks resale velocity in each Valencia phase, he alerts sellers when a neighbor’s pending renovation might distort comps, guarding equity before the listing hits MLS.

If your next chapter includes sunshine without yard work, Katz turns red tape into a welcome-home ribbon.

5. Tricoli Team – review-backed hustle for growing families

Gated living is not always about chandeliers and marble. Sometimes it is a safe cul-de-sac where bikes roam and the PTA meets at the clubhouse. For that slice of suburbia, families trust Jeff Tricoli’s Keller Williams squad.

Two thousand five-star reviews tell the story: constant availability and data-driven pricing. Tricoli agents cover the county daily, moving from Canyon Trails to Nautica Lakes with clockwork efficiency. The effort pays off. They have logged more than three hundred gated closings across price points, spotting appraisal traps and HOA quirks that can derail FHA loans.

Speed is their edge. Internal numbers show their listings sell eight percent faster than the county average, thanks to focused staging advice and social ads that reach buyers within five miles of each gate. Yet the process never feels rushed. Clients recall late-night calls that walk through estoppel letters line by line, preventing fee surprises at closing.

Need a team that can open kid-friendly gates on short notice and still negotiate with precision? Tricoli already has the key fobs ready.

6. Alex & Margot Platt – social-savvy partners for new luxury

GL Homes keeps rolling out modern playgrounds like Lotus and Boca Bridges, and the Platts sell them almost as quickly as the slabs cure. This Compass duo landed on Palm Beach County’s forty-under-forty list by pairing scroll-stopping video tours with concierge-level service.

Margot’s design degree shows in every listing. She tweaks furniture angles, records a one-minute reel, and often tops five thousand views before sunset. Alex studies inventory velocity and nudges price bands so offers arrive within days. Together they have closed more than sixty gated deals, most north of one million dollars, while preserving a spotless five-star review streak.

Their edge is relatability. They juggle toddlers, know which HOAs host stroller parades, and recite school rezoning updates between showings. Remote buyers value live video walk-throughs that linger on cabinet hinges, gate call boxes, and cell-service dead zones.

If your wish list reads “brand-new, smart-home, resort amenities, zero maintenance,” the Platts will have a virtual key waiting before your plane lands.

7. Martha W. Jolicoeur – Wellington’s equestrian whisperer

Million-dollar horses fly into Wellington each winter, and Martha Jolicoeur welcomes their owners. A former Grand Prix rider, she sells gated estates the way trainers pick Olympic mounts: footing, flow, and flawless condition.

Her card reads Douglas Elliman, but her real office is the bridle path. Buyers follow her golf cart through Palm Beach Point or the Aero Club while she explains which HOA bylaws set barn height, runway access, and manure pickup. That detail work seals deals before offers hit paper; no one wants a zoning surprise when a forty-stall barn is at stake.

Production matches reputation. Jolicoeur ranks among Elliman’s top Florida agents, recording single-estate sales above $15 million while still sponsoring the Great Charity Challenge at the Winter Equestrian Festival. Clients say she negotiates like a show jumper at the final fence: fast, fearless, and precise.

If your dream home includes a tack room and space for a Gulfstream, Jolicoeur already has the gate code.

How we chose the seven gatekeepers

You deserve more than a popularity contest, so we reviewed license records, MLS data, and thousands of verified reviews to find agents who excel inside gated walls, not just generic ZIP codes.

We began by mapping every Palm Beach sale from 2021 through 2024 that required an HOA gate code. Volume carried the most weight; one broker logged $636 million behind a single guardhouse, proving that niche experience matters.

Client satisfaction came next. We looked for hundreds of five-star reviews, a sign of consistent service rather than hand-picked praise.

Local expertise also counted. Board memberships, resident status, and years of blogging showed that a broker can explain pet limits, equity buy-ins, and flood-zone rules without outside help.

We finished with negotiation results: days on market, list-to-sale ratios, and record prices. Community involvement, such as sponsoring clubhouse charities or mentoring HOA boards, served as a bonus tie-breaker.

The result is a roster that covers luxury yachts, pickleball capitals, and bridle paths, so whatever your lifestyle, one of these seven already speaks your language.

What to expect when buying in a gated community

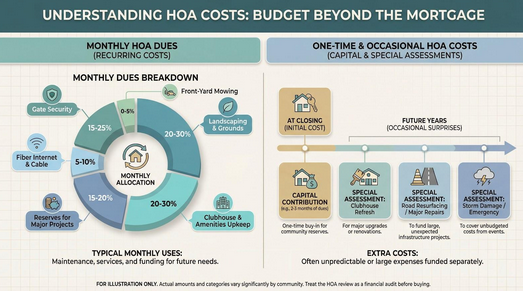

HOA fees and assessments, budget beyond the mortgage

Start with the number no one posts on the listing photos: monthly dues. In Palm Beach County, basic gated neighborhoods charge about three to four hundred dollars each month. Step into a country-club enclave and that figure can top one thousand before you add optional golf equity.

What do those dollars cover? Think of them as a bundled service plan. Dues usually pay for gate security, common-area landscaping, clubhouse upkeep, and reserves for large projects such as road resurfacing. In newer master-planned communities, the fee may also include fiber-optic internet or front-yard mowing.

The bigger shock often hides in capital contributions and special assessments. Many associations collect two or three months of dues at closing to build reserves. Others impose one-time “clubhouse refresh” fees when renovation funds run short. Savvy agents preview those costs early and, when possible, negotiate credits so the final statement does not surprise you.

Rule of thumb: request the association’s latest budget and reserve study as soon as you go under contract. A healthy reserve, typically at least seventy percent of projected needs, signals stable dues. A thin reserve paired with aging amenities hints at future increases. Your Realtor should translate those spreadsheets into plain language and an annual cost you can add to everyday expenses.

Treat the HOA interview like a financial audit. Clear numbers make the move from offer to welcome packet smoother.

HOA rules and everyday lifestyle, read the fine print before you sign

Security gates provide the first layer of order; the bylaws supply the rest. Some boards dictate roof colors, mailbox designs, and even the length of time a guest’s vehicle may remain in the driveway. Others focus only on speed limits and quiet hours after ten.

Rules shape daily living, so treat them like a second set of property specs. Dog lover? Check weight limits—many boards cap pups at forty pounds. Planning to rent seasonally? Some communities require twelve-month minimum leases or ban short-term rentals completely.

Retiree enclaves add another layer: age restrictions. A fifty-five-plus neighborhood requires at least one resident to meet that mark, and visits by minors may be limited to thirty days each year. Break the rule and you face fines or, worse, forced relocation.

Ask your agent for a bylaws cheat sheet during showings. Skilled gated specialists flag quirks that conflict with your lifestyle before you fall for the granite countertops, saving both heartache and hefty violation fees.

Access and privacy, why a Realtor is your golden ticket

Iron gates do more than impress visitors; they also keep casual shoppers out. Most communities need the listing agent to register your name, and many refuse entry to unescorted guests, even during open houses. Arrive without clearance and you may spend your visit at the guard kiosk instead of touring the kitchen.

The rule protects owners but blocks last-minute drive-bys. Top gated specialists turn that barrier into an advantage. They group several showings under one security clearance, submitting your identification twenty-four hours ahead so you glide through like a member.

Inside, privacy rules tighten further. Clubhouses often ban photography, streets carry twenty-five-mile speed limits, and “no solicitation” policies prevent door-knocking for neighbor intel. A well-connected agent fills that gap, sharing inside chatter on upcoming listings or pending assessments while you cruise the boulevard.

Treat your Realtor as both tour guide and passport. The smoother they manage gate access, the faster you move from visitor log to resident roster.

Be aware of 2024–2026 rule changes

Buyer-agent commissions just flipped

For decades sellers quietly included the buyer-agent fee in the list price. A landmark 2024 settlement ended that habit. Sellers no longer must pre-pay your agent, and you must sign a written agreement that spells out how your representative is paid.

What changes on the ground? During showings you will now see a blank or variable field where “buyer commission” once appeared. Some sellers still offer a full fee to widen the pool, others offer half, and a few offer none. Before your first tour, your agent should explain three funding options:

- Negotiate the fee into the purchase price when inventory is plentiful.

- Request a closing credit from the seller earmarked for your agent.

- Pay the commission yourself; many lenders now allow it to roll into the mortgage if the appraisal supports the higher figure.

Clear math at the start avoids awkward haggling later. Experienced gated specialists already have lender scripts to keep deals moving under the new model.

Florida’s new HOA law reins in heavy-handed boards

Good news for owners tired of constant violation letters: Tallahassee narrowed association powers in late 2025. The reform caps excessive fines, demands transparent budgeting, and requires boards to open more records to members. An association that once charged fifty dollars a day for a visible trash can must now justify the penalty.

Why does this matter when you buy? Financial clarity. Sellers must disclose unpaid fines, and boards must explain fee hikes with documented needs. Your agent should pull the latest budget minutes and any pending special-assessment votes. If the numbers look weak, negotiate a price concession or keep shopping.

The law also shortens the record-request timeline, so you can review reserve health in days, not weeks. A sharp Realtor will use the statute to secure documents early, shrinking both risk and stress.

Insurance and storm-hardening, budget for wind before it blows

Florida premiums climbed faster than sea-level projections, and gated homes feel the pinch. Carriers reward impact windows, reinforced garage doors, and wind-mitigated roofs with sizable discounts, while dated features can spike quotes or force owners into the high-risk pool.

The state revived the My Safe Florida Home grant in 2025, offering up to ten thousand dollars for storm upgrades. Sellers who already used the program often advertise “grant complete” as a selling perk; buyers still have funds available if the property lacks shutters or a fortified roof deck.

Ask your agent for a recent wind-mitigation report and roof age before you sign. A ten-year-old tile roof with clips and a secondary water barrier can shave thousands off annual premiums compared with a fifteen-year-old roof missing that paperwork. Savvy Realtors line up quotes during inspection week so you can weigh true carrying costs beside the mortgage.

The cheapest time to think about hurricanes is before closing. Lock in the right coverage and improvements now, then follow the next storm update with more confidence and a smaller deductible.

Tips for touring and choosing gated community homes

Schedule first, stroll later

Call it the golden rule of gated shopping: plan before you drive. Guards need your name in the log a day ahead, and residents value quiet streets. Work with your agent to bundle three or four homes under one security clearance so you spend more time in foyers and less time at kiosks.

Evaluate the community, not just the kitchen

Granite counters impress, but shared spaces protect value. During the tour, linger in the clubhouse, test gym machines, and note whether tennis courts show cracks or fresh paint. Well-kept amenities signal healthy reserves and boards that spend dues wisely.

Read the fee sheet line by line

Ask for the HOA disclosure summary; Florida law requires sellers to provide it. Scan for hidden costs such as capital contributions, transfer fees, and golf-equity buy-ins that dwarf monthly dues. A sharp Realtor will translate the jargon and estimate your annual true cost.

Ask about future assessments

That resort-style pool may be due for resurfacing. Boards often discuss big projects years in advance. Request minutes from the last two board meetings; they reveal looming expenses that could trigger assessments soon after you unpack.

Bring the right ID and a phone charger

Many gates scan driver’s licenses and photograph tags. Forget yours and the tour stalls. Inside, cell service can dip, so carry a charger or portable hotspot if you plan to video chat a spouse or inspector.

Tap your agent’s vendor list

Once you fall for a home, you will need HOA-approved painters, landscapers, and pool services. Seasoned gated specialists keep a vetted roster that meets insurance rules, saving you trial and error.

Conclusion

Choose carefully, lean on expert guidance, and the right gated address will feel like a permanent holiday with your name on the resident list at the front gate.

Is It Time to Buy? Exploring the Value of Homeownership for Investors

Choosing to purchase a property can be a significant decision that can align your financial and lifestyle goals. For landlords and investors, the ability to purchase your a home is an opportunity to acquire wealth while also providing you with stability and control over your living situation. In many cases, homeowners also explore using part of their property as flexible office space for small business operations or tenants, which can further increase its value.

Read this article as we outline the reasons why owning a home will help you develop long-term goals. This includes major points to think about before transitioning from renting to ownership, particularly in Bucks County’s evolving property market, where more people are even converting basements, studios, or outbuildings into office space for business use.

Financial Benefits of Owning a Home

Owning a home offers numerous financial benefits that can enhance your financial security. Compared to renting, home ownership generally provides many ways to create wealth, build equity, enjoy tax benefits, and have predictable monthly payments. For some owners, it also opens the door to earning passive income by renting out office space to local entrepreneurs.

Building Equity

When you buy and own a house, a portion of your mortgage payment goes each month to reducing the loan balance and increasing your equity, or the portion of your home you own.

Instead of paying rent to a landlord, you are increasing wealth through equity, which is a form of forced savings. Your equity increases as you pay your mortgage down, and your home’s value can potentially increase. Some homeowners even use this equity later to expand home office space or create rental office suites for small businesses.

Over time, equity can become an asset you can borrow against. When you sell a property, you hopefully sell for a profit, rather than simply handing a landlord your hard-earned money each month.

Tax Benefits

Typically, homeownership comes with tax deductions, which renters do not receive. You will most likely be able to deduct your mortgage interest and property taxes from your income tax, thereby lowering your taxable income.

Plus, if you sell your house after living in it for a specific amount of time, you might also receive exemptions from capital gains taxes and other tax benefits. Homeowners who use a portion of their home as office space may also qualify for additional deductions. All of these tax benefits will help you save a lot of money and help you keep track of homeownership costs.

Stable Monthly Payments

If you have a home with a fixed-rate mortgage, then your monthly principal and interest are established for the life of the loan. So you can forecast your financial situation with great certainty.

While rents can increase each year based on market conditions and landlord decisions, a fixed mortgage payment keeps your housing costs steady and manageable over the long term. This stability is particularly beneficial for people running a home-based business who rely on predictable expenses.

Lifestyle Benefits of Homeownership

There are benefits to owning a home beyond financial investment. Homeownership gives you stability, freedom, and a sense of community. These qualities help improve your quality of life and personal satisfaction, something renting often can’t provide. Homeowners also enjoy the flexibility to convert rooms into office space or creative studios without needing approval from anyone.

Stability and Control Over Your Living Space

Stability and control over your living space are important benefits of owning a home. Living situations change all the time with renting. But with ownership, you have the ability to stay as long as you want.

This stability will lower your overall stress, allowing you to have an enriched, stress-free living arrangement for you and your family—plus the freedom to plan long-term office or workspace needs if you run a business from home.

Freedom to Customize and Renovate

Homeownership allows you to make your home yours in terms of style or functionality. You can paint the walls, remodel a room, change the fixtures, and design the yard in a way that suits your needs, and you do not have to ask for permission.

These upgrades not only enhance your day-to-day living, but they also enhance the value of your property. Many homeowners creatively repurpose garages, lofts, or spare bedrooms into office space for tenants or small business operations. With that freedom of ownership, you can create a home that fits your tastes and lifestyle.

Sense of Belonging and Community

Homeowners tend to stay in a place longer than renters, giving them the time to build relationships with people in their neighborhood, as well as engage with their community.

Building those relationships and engaging with your community can enhance your quality of life and serve as a valuable support network if the need arises. For families with children or anyone seeking a stable living environment, having a sense of connection with a community is crucial. This is also beneficial for local small businesses, as homeowners who operate home offices often rely on nearby services and partner with nearby entrepreneurs.

Pride of Ownership and Personal Satisfaction

There is a unique pride when you own your home. It represents accomplishment and security, a milestone many people strive for. This pride can inspire you to take better care of your property and neighborhood. The feeling of having a place to call your own, tailored by your choices, brings a deep sense of personal satisfaction and emotional comfort.

How Homeownership Builds Long-Term Wealth

Creating wealth is more than just putting money into a bank account; it’s about building assets that appreciate over time. Owning a home gives you options for long-term wealth appreciation that renting does not—and this includes the possibility of generating extra income through renting office space to small business tenants.

1. Building Equity with Every Payment

Each mortgage payment goes towards building your ownership interest, also referred to as equity, in your home. When you pay rent, that money is gone, but mortgage payments increase your wealth.

As you pay down your loan and your home appreciates, you are growing your equity. You can borrow against that equity later for larger expenditures, use it as collateral for other loans, or, if you sell the house, you can take it as cash. Some owners leverage this equity to build accessory structures or private office pods to rent out.

2. Property Value Appreciation

Most homes will rise in value with time, a phenomenon known as long-term appreciation. Keep in mind that local markets can fluctuate; however, as a long-term investment, you will likely benefit from your home.

Additionally, there are many avenues to increasing your home’s value. Most often, being in a developing area alone will have a positive impact on your home’s value. The same for making improvements to your home—including adding or upgrading office space, which has become increasingly in demand among remote workers and small business owners.

3. Leveraging Home Equity for Other Investments

A home equity line of credit (HELOC) is a loan that allows homeowners to borrow on the equity of their home, often at a lower interest rate than other loan types, to finance renovations, start a business, emergency expenses, or increase their real estate portfolio.

Some homeowners use HELOC funds specifically to create professional office space, coworking rooms, or rental spaces for entrepreneurs, turning their home into a dual-purpose financial asset.

4. Tax Advantages

Another important thing about homeownership is that it offers tax benefits. You may also be able to deduct mortgage interest and property taxes, and if you sell your home after living in it for some time, you may not have to pay taxes on some or all of your profit.

Tax benefits allow you to keep more of your money, which increases your ability to save or invest somewhere else. Home office deductions can also reduce costs for homeowners running small businesses.

5. Generational Wealth

Homeownership can also create opportunities for your family. As you build equity and benefit from appreciation, you are giving yourself the chance to pass on wealth generationally. This is why homeownership remains a crucial means of achieving and maintaining long-term financial stability for you and your loved ones.

What to Consider Before Making the Transition from Renting to Buying

Before making the move from renting to owning, it’s important to explore all aspects of making a wise home purchase. A little foresight will help you avoid surprises and make informed decisions regarding a property that will contribute to your financial and lifestyle goals. This includes considering whether you plan to use part of your home as office space or rent workspace to tenants.

Assess Your Financial Readiness

First off, take a good look at your budget, income, and credit score. You will need enough savings for your down payment, closing costs, and expenses associated with moving from where you live now to your new home.

Lenders will take a close look at your debt-to-income ratio and your credit history, too. Knowing where you stand financially will help you form realistic expectations and avoid a situation where you’re financially “house poor.” Make sure to truly account not only for the purchase, but also for the ongoing costs of home ownership—and any additional expenses if you plan to build or rent out office space.

Understand the Responsibilities of Owning a Home

As a homeowner, you are responsible for everything. You will be responsible for routine maintenance and yard work, as well as emergency repairs. If your roof starts to leak or your furnace breaks, it’s up to you to get it taken care of.

This is why many homeowners utilize property management services to keep their investment in good shape. From routine maintenance to emergency repairs, Northern Virginia property managers ensure properties stay in top condition. They can also advise homeowners who want to safely rent office space to tenants or small business operators.

Consider Local Market Conditions

The real estate market differs widely from one place to the next. Before you buy, take time to learn about housing values, trends, and demand in your area, such as Bucks County. Some neighborhoods may give you better long-term value, while others may have a solid and steady value or may be more affordable. Local demand for home-based office space or mixed-use properties can also affect your decision.

Think About Your Long-Term Plans

How long do you think you’ll be in one place? If you anticipate moving in a few years, buying may not be a very good financial choice due to the costs of buying and selling a home.

But if you’re planning to settle in for the long haul, homeownership makes more sense and is likely to pay greater rewards in the long run. This permanence also makes it easier to relocate your business to this permanent spot and establish a brand name.

Work With Property Management Experts

If you are an investor or would just like an easier experience, utilizing a property management company can remove the stress of maintaining your new property.

These people can take care of repairs, find you tenants (if you are renting part of the property), and help you meet the different legal requirements that will protect your investment and peace of mind. They can even help manage office-space tenants if you choose to rent workspace to small businesses.

Conclusion

Buying a home is a big decision that has benefits both financially and from a lifestyle perspective for building wealth. There are obligations to home ownership, so you need to be ready and understand your area and requirements before making your move.

Home ownership offers attention and capabilities for growth that no rental situation can ever offer. With good planning and expert guidance, anyone, whether you are a landlord, an investor, or a tenant who wants to one day own a home, can benefit from home ownership—including those exploring creative ways to integrate office space, support small business operations, or generate additional income from workspace rentals.

When and Why to Reassess Your Real Estate Tax Strategy

If you own rental properties or have dipped your toes into real estate investing, you probably know that taxes can be both a helpful tool and a bit of a headache. Many investors set up a tax plan early on and figure it will carry them through for years. The truth is that real estate moves quickly. Your tax strategy should move with it. Reassessing it from time to time can help you keep more of your returns and avoid surprises when tax season rolls around.

Below are some key moments and reasons that signal it might be time to take another look at your approach.

When Your Portfolio Grows or Changes

A lot of investors start off with one small rental and slowly build from there. As your portfolio expands, your tax picture becomes more complicated. The deductions grow. The depreciation schedule gets longer. You might even find yourself investing in different types of properties like short term rentals or commercial units. Each one plays by slightly different tax rules.

If your portfolio looks very different today than it did a couple of years ago, that is a clear sign to reevaluate your tax plan. Even adding one new property can change your cash flow enough to justify a new strategy. A quick check in with a tax professional can help make sure you are not leaving money on the table.

When Tax Laws Shift

Tax laws do not stand still for long. Every few years there are changes to depreciation rules, bonus depreciation, capital gains rules or 1031 exchange guidelines. These changes can have a real impact on the timing of your sales, the way you structure your purchases and even how you manage your properties on a daily basis.

If the IRS updates something and you have not updated your strategy since then, you might miss out on opportunities or pay more than you need to. Paying attention to these shifts is a smart way to keep your plan fresh. Even a brief consultation with a CPA can show you what changed and how much it affects you.

When You Are Planning a Sale or Exchange

Selling a property is one of the moments when tax planning becomes very important. If you want to reduce your tax bill, the timing matters more than many investors expect. A 1031 exchange is a great tool, but it comes with its own set of rules and deadlines. Planning ahead makes the process much easier and also helps you avoid common pitfalls.

For example, some investors choose to update their strategy because they want to avoid depreciation recapture. This topic trips up many people because it feels hidden until the numbers show up on a tax return. Understanding how it works and preparing for it early can help you keep more of your gains and stress a whole lot less on closing day.

When Your Personal or Business Goals Change

Life changes. Maybe you switched jobs, moved to a different state or brought on a partner for your real estate ventures. Any of these shifts can affect your taxes. Different states have their own rules and credits. Partners change your filing decisions. Even your long term goals matter. If your focus has shifted toward income stability instead of rapid growth, your tax strategy should match that.

It is completely normal for your priorities to change over time. A regular check in makes sure your tax approach still fits your real life.

A Good Rule of Thumb

Most investors benefit from revisiting their real estate tax strategy every year or two. It does not have to be a huge project. Think of it like routine maintenance. A little attention now can prevent bigger issues later. And you might discover new opportunities or deductions you did not know you could use.

If you stay flexible and review things when life or the law changes, you can build a healthier and far more predictable tax picture for the long term.

Hidden Costs of Commercial Building Ownership: Ongoing Maintenance Items You Should Consider

Understanding the True Cost of Commercial Building Ownership

Commercial building ownership entails financial obligations that extend far beyond the initial purchase or construction cost. The true cost of ownership involves ongoing expenditures that are often underestimated but are critical to maintaining the building’s functionality, value, and compliance with regulatory standards. These costs occur throughout the lifespan of the property and can increase significantly over time if not addressed proactively.

Regular Maintenance and Repairs

One major component of commercial building ownership is regular maintenance. Building systems such as plumbing, electrical wiring, and HVAC require periodic inspections and servicing to ensure they continue operating efficiently. Without these routine checks, small issues can escalate into costly repairs. Owners must factor in expenses like replacing aging equipment, repairing structural damage, or addressing issues like water leaks or foundation cracks.

Energy Efficiency and Utility Costs

Energy consumption is another recurring cost that impacts long-term ownership expenses. Older buildings often feature outdated systems that are inefficient and expensive to operate. Retrofitting buildings with energy-efficient systems, such as LED lighting or solar panels, can reduce utility costs but may require substantial upfront investment. Tracking energy usage with advanced monitoring tools allows owners to make informed improvements but adds to ongoing budget considerations.

Compliance with Regulations

Adhering to building codes and local regulations often incurs additional costs. Requirements may include safety inspections, fire suppression system upgrades, and accessibility improvements to meet ADA standards. Periodic updates to regulations can necessitate modifications to the property, and the costs of failing to comply can result in fines or even legal penalties.

Insurance and Liability

Insurance coverage is essential for mitigating risks associated with commercial building ownership. Policies for fire, flood, theft, or liability claims often increase annually and must account for fluctuating property values or local risk factors. Likewise, liability from incidents onsite—such as accidents involving tenants or visitors—can lead to additional unexpected costs requiring careful coverage and management.

Renovations and Modernization

Over time, commercial properties often need modernization to remain competitive in the market. Renovations may include updating interior designs, adding technological features, or upgrading materials to ensure durability. In food-prep areas, cafés, or office pantries, a kitchen tile backsplash is a simple, durable upgrade that protects walls from moisture and makes ongoing cleaning easier—helping control long-term maintenance costs.These improvement costs can be substantial, particularly if they involve major reconfigurations or addressing outdated infrastructure. Owners must prepare for these expenses in advance.

Environmental and Landscaping Concerns

Proper care of the property’s surrounding environment is an ongoing concern. Landscaping upkeep, waste management, and pest control can generate recurring costs. Additionally, buildings in areas prone to extreme weather conditions may require storm-proofing or repairs to limit environmental damage, further adding to maintenance costs.

By understanding these hidden and ongoing expenses, owners can better anticipate the true financial commitment associated with commercial building ownership. An informed approach to these costs can ensure proper budgeting and help preserve the value of the property.

Routine Maintenance Expenses: What You Need to Know

Routine maintenance expenses are a critical aspect of commercial building ownership that can significantly impact operating budgets. These recurring costs are necessary to ensure the property remains functional, safe, and compliant with regulations. Building owners must plan for these expenses to avoid unexpected financial strain and to safeguard their investment.

Key Areas of Routine Maintenance

- HVAC Systems Heating, ventilation, and air conditioning require regular servicing to ensure optimal performance. Tasks such as filter replacement, checking refrigerant levels, cleaning ducts, and inspecting components can prevent costly breakdowns and prolong system lifespan.

- Plumbing Maintenance Routine attention to plumbing systems can prevent leaks, water damage, and costly repairs. Activities like clearing drains, inspecting pipes for corrosion, and maintaining water heaters often fall under these expenses.

- Electrical Systems Commercial buildings require regular inspections of wiring, outlets, lighting systems, and circuit breakers to prevent fire hazards and ensure compliance with safety codes.

- Roof Inspection and Repairs The roof is a critical structure that protects the building from weather damage. Regular inspections for leaks, cracks, and issues with drainage systems are necessary to avoid severe damage and expensive replacement costs.Pro tip: Get A Yearly Roof Inspection To Ensure No Surprises Later On.

Periodic Inspections and Cleaning

- Fire Safety Equipment Fire alarms, extinguishers, sprinkler systems, and emergency lighting should be inspected and tested regularly to remain operational during emergencies and meet legal requirements.

- Exterior Cleaning and Landscaping Routine maintenance of building exteriors, such as power washing, window cleaning, and upkeep of landscaping, contributes to curb appeal while preventing wear and tear damage.

- Pest Control Ongoing pest management ensures the property remains free from rodents, insects, and other nuisances that could damage infrastructure and harm tenant satisfaction.

- Gutter Cleaning: Commercial buildings have a lot of square footage and as a result they collect more rain water, if your gutter systems are clogged this could mean hundreds of gallons of water getting into places they shouldn’t and causing major damage. To avoid this, we recommend getting commercial gutter cleaning 2-3x per year.

Addressing Wear and Tear

General wear and tear on flooring, paint, fixtures, and furniture should also be included in the maintenance budget. These items, while appearing minor, can accumulate substantial costs over time if neglected, impacting both functionality and aesthetics.

In commercial kitchens, break rooms, and food-prep areas, installing kitchen backsplash tiles can help protect walls from stains and moisture while reducing repainting and long-term maintenance costs.

Maintaining a detailed plan that outlines the frequency of inspections and servicing for each category is vital. Without proactive measures, repairs or replacements can escalate, causing bigger financial burdens.

Unplanned Repairs: Preparing for the Unexpected

Unplanned repairs are an inevitable aspect of commercial building ownership and can arise at any time due to unexpected circumstances. These repairs often stem from unforeseen issues such as equipment failure, structural damage, extreme weather events, or even tenant-related problems. Owners must be prepared to address such situations swiftly to prevent further damage, protect the building’s integrity, and minimize disruptions to business operations.

Key areas where unexpected repairs frequently occur include:

- HVAC System Breakdowns: Heating, ventilation, and air conditioning systems are critical for occupant comfort. Mechanical failures can be sudden and costly, especially if emergency repairs or replacements are needed. Deferred maintenance often exacerbates these problems.

- Plumbing Emergencies: Burst pipes, leaks, or flooding can cause significant damage to interiors and lead to high water bills or mold growth. Repairing or replacing defective plumbing systems quickly is essential to curbing further issues.

- Roof Damage: Severe weather conditions, such as heavy snow, high winds, or hail, can compromise the roof’s structural integrity. Repairs might range from patching leaks to complete roof replacements depending on the severity of the situation.

- Electrical Failures: Outdated wiring, overloaded circuits, or power surges can result in blackout scenarios or fire hazards. Unaddressed electrical issues create serious safety risks and may necessitate costly upgrades.

- Foundation Cracks or Settling: Subtle foundation issues can escalate into significant structural problems, jeopardizing the stability of the building. Addressing these issues as soon as they are detected is crucial.

Owners should maintain a financial cushion, such as a contingency fund, specifically for addressing unexpected repair needs. A proactive approach that includes regular inspections, predictive maintenance tools, and strong vendor relationships can mitigate the impact of sudden repair demands.

Energy Efficiency and Utility Management Costs

Energy efficiency and utility management represent critical aspects of commercial building ownership. These costs are often overlooked but can significantly affect a property’s operating budget over time. Building owners face recurring expenses associated with electricity, gas, water, and waste management services. Additionally, regulatory requirements and energy standards often mandate upgrades that impact utility expenditures further.

One primary factor influencing energy costs is the building’s mechanical systems, such as heating, ventilation, and air conditioning (HVAC) units. Inefficient or outdated HVAC systems can result in excessive energy consumption, leading to higher utility bills. Maintenance of these systems is essential to optimize energy usage, and this typically involves tasks such as filter replacements, duct cleaning, and thermostat recalibrations.

Lighting systems also play a significant role in energy efficiency. Older fluorescent lighting may require replacement with energy-efficient LED alternatives to reduce electricity consumption. The initial installation of such upgrades can be costly, but the decreased energy usage over time offsets these expenses.

Water consumption and waste management contribute to utility costs as well. Fixture leaks, outdated plumbing systems, and inefficient appliances can lead to unnecessary water loss. Implementing water-saving solutions, such as low-flow faucets and modern toilets, can improve efficiency. Furthermore, managing waste disposal contracts and ensuring compliance with local recycling regulations add to ongoing operating expenses.

Building energy audits may be required periodically to identify inefficiencies and recommend improvements. These audits, while useful, often necessitate additional expenses for both assessment and implementation. By understanding these utility and energy efficiency costs, building owners can better allocate resources to maintain overall operational effectiveness.

Hidden Costs of Landscaping and Outdoor Maintenance

Landscaping and outdoor maintenance can contribute significantly to the recurring expenses of owning a commercial building. While the visual appeal of well-maintained grounds is essential for attracting tenants and clients, this comes with numerous hidden costs that property owners must anticipate.

Regular lawn care services, including mowing, fertilizing, aeration, and reseeding, are necessary to ensure healthy grass coverage. Additional costs may arise during seasonal changes, such as leaf removal in autumn or snow removal in winter. Hardscape maintenance—including cleaning, pressure washing, and sealing of walkways, patios, or parking areas—also adds to the upkeep.

Tree and shrub care requires regular attention to prevent overgrowth and maintain safety. Pruning, pest control, and the occasional tree removal or stump grinding contribute to these costs. Furthermore, irrigation systems need regular inspections, repairs, and seasonal adjustments. A malfunctioning irrigation system can result in water wastage and higher utility bills.

Property owners may also face city or local regulations regarding outdoor areas. Compliance costs could include tree planting mandates, erosion control measures, or handling drainage systems. Delays or violations may incur additional expenses, including fines or rework fees.

Outdoor lighting and signage also require ongoing care. Regular bulb replacement, electrical repairs, and weatherproofing are indispensable to keep these fixtures functional and visually appealing. Additionally, decorative features like fountains or retaining walls demand occasional repairs and preventive maintenance.

Environmental factors such as droughts, flooding, or extreme weather conditions can escalate these expenses unpredictably. Restoring damaged vegetation or structures often leads to significant unplanned expenditures. These ongoing challenges make it crucial to budget adequately for landscaping and outdoor maintenance.

Technology and Security System Upgrades

Commercial building ownership involves keeping pace with advancing technology and security needs. In today’s highly digitalized world, outdated systems can be a hidden expense, requiring periodic upgrades to ensure efficiency, compliance, and safety. Building owners must factor in the costs of maintaining modern technology to keep their property competitive and secure.

Common Technology Upgrades to Consider

- Access Control Systems: Older key-based locks are increasingly replaced by sophisticated access control systems using biometric authentication, keycards, or mobile-based technology. These systems demand regular software updates and occasional hardware replacements.

- Building Management Systems (BMS): To optimize energy usage and monitor systems like HVAC, lighting, and water usage, BMS solutions are evolving. Upgrades often entail installing new sensors, upgrading software, or integrating IoT solutions for better performance.

- Internet Connectivity Infrastructure: Many tenants expect fast, reliable internet service. Building owners may need to invest in fiber-optic cables, Wi-Fi network enhancements, or even dedicated data centers to meet demand.

Security System Enhancements

Maintaining security is paramount for any commercial building. Evolving threats, both physical and cyber, push owners to implement robust solutions.

- Camera Systems: High-definition cameras with AI analytics now replace basic surveillance cameras. Continuous improvements in resolution, storage capabilities, and monitoring tools require periodic investments.

- Cybersecurity Measures: Buildings equipped with smart technologies face increasing risks of cyberattacks. Regular penetration testing, software updates, and installation of firewalls or encryption tools are vital.

- Alarm Systems: Integrating wireless alarms, smart sensors, and remote monitoring features allows property owners to identify threats quickly. These upgrades also increase tenant confidence and reduce liability risks.

Tips for Effectively Budgeting for Maintenance Expenses

Maintaining a commercial building requires meticulous financial planning to avoid unexpected expenses. Budgeting effectively for ongoing maintenance can prevent costly disruptions and ensure the property remains functional and efficient. Here are several tips to manage maintenance expenses either proactively or strategically:

1. Conduct a Comprehensive Building Assessment

- Evaluate the property’s current condition, including structural elements, electrical systems, HVAC units, plumbing, and exterior features.

- Identify components that may require frequent repairs or replacement based on their age or usage level.

- Establish a prioritized list of areas needing attention, which can guide resource allocation for maintenance spending.

2. Categorize Maintenance Costs

- Break down expenses into preventive maintenance, minor repairs, and major replacements to ensure funds are allocated accordingly.

- Plan separately for seasonal expenditures, such as snow removal in winter or landscaping costs during warmer months.

- Review historical financial data to identify patterns in maintenance costs and use it for future projections.

3. Allocate Funds for Unforeseen Repairs

- Create an emergency reserve fund specifically for unexpected repairs, such as a leaking roof or a sudden plumbing failure.

- Assess industry norms and set aside a percentage of annual property income for these unanticipated expenses.

4. Utilize Technology for Improvement

- Invest in software to track maintenance schedules, monitor costs, and set reminders for preventive maintenance tasks.

- Using tech tools can help efficiently anticipate expenses and avoid delays in addressing potential problems.

5. Work with Professional Inspectors

- Schedule regular professional evaluations of the building to identify issues early.

- Inspectors can provide insights on potential wear and tear or safety hazards, which assists in planning repairs before the costs escalate.

6. Negotiate Service Contracts

- Establish long-term contracts with service providers for HVAC, plumbing, and electrical system maintenance. Bulk agreements often reduce per-service costs.

- Compare maintenance providers and request quotes to secure competitive rates without sacrificing quality.

7. Incorporate Long-Term Goals

- Factor in capital improvements, such as energy-efficient upgrades or modernized equipment, to reduce operating expenses over time.

- Plan maintenance in alignment with long-term strategies to boost building value while controlling costs.

8. Review Budget Regularly

- Revisit the maintenance budget periodically in response to fluctuating material costs, labor rates, or changes in occupancy patterns.

- Adjust allocations to ensure alignment with the actual needs of the property and the market.

By implementing these strategies, property owners can better anticipate regular and unexpected maintenance expenditures, reducing financial strain and safeguarding the longevity of their commercial building assets.

Key Takeaways and Final Thoughts on Hidden Costs

Commercial building ownership comes with a myriad of hidden costs that extend beyond the initial purchase price or mortgage payments. Owners often encounter ongoing maintenance obligations that can escalate over time, impacting profitability and financial planning. Recognizing these potential expenses can aid in better budgeting and long-term decision-making.

Unexpected Maintenance Challenges

- Structural Repairs: Issues like foundation cracks, roof leaks, or aging support beams may require unexpected interventions that demand substantial investment.

- HVAC System Wear and Tear: Heating, ventilation, and air conditioning systems often face periodic breakdowns or performance reductions. These systems may require regular servicing, filter replacements, or even full system upgrades.

- Plumbing System Decline: Older buildings could be prone to plumbing issues, such as pipe corrosion or inefficient water fixtures, leading to increased water costs and repair bills.

- Electrical Upgrades: With changing technologies, older electrical systems may need upgrading to accommodate modern energy demands, increasing maintenance costs.

Recurring Operational Expenses

- Utility Costs: Utilities such as electricity and water may vary monthly and rise significantly during periods of high use, especially if systems are outdated or inefficient.

- Safety Compliance: Regular inspections to ensure compliance with safety, fire codes, or environmental regulations can trigger costs for repairs or upgrades dictated by new standards.

- Commercial Insurance Premiums: Coverage for commercial properties can increase based on risk factors and unexpected ownership liabilities.

Proactive Measures to Mitigate Costs

- Performing routine inspections can help identify problems early, reducing the financial burden of more significant, unexpected repairs.

- Investing in energy-efficient upgrades and eco-friendly systems can lower long-term operating costs while improving building sustainability.

- Allocating a reserve fund specifically for maintenance and repairs ensures access to financial resources when needed.

Vendor and Professional Fees

- Contracting reliable property management companies and commercial maintenance professionals can streamline upkeep, but their services often come at a premium. Owners must weigh the benefits of outsourcing while staying mindful of costs.

Understanding these elements of hidden costs allows a more proactive approach, ensuring smoother operations and fewer surprise expenditures over the lifetime of commercial building ownership.

How Good Accounting Secures Better Lease Deals

Leasing is often one of the biggest expenses for businesses, whether it’s office space, retail storefronts, or industrial warehouses. While most owners think about location, square footage, or amenities, what often gets overlooked is how much good accounting can influence negotiations. Landlords and leasing companies care about numbers—your financials tell a story about your stability, reliability, and growth potential. Having clear, accurate books can be the difference between landing a favorable lease deal or being saddled with higher costs.

Why Accounting and Leasing Go Hand in Hand

A lease is a long-term financial commitment. Landlords aren’t just renting out a space—they’re trusting that your business can pay on time for years. Strong accounting practices prove that you’re a low-risk tenant. On the other hand, sloppy records or vague financials raise red flags. According to Deloitte, 57% of landlords say financial transparency is one of the top factors they consider in lease approvals. This makes accounting more than just compliance—it’s a bargaining tool.

How Proper Accounting Strengthens Negotiations

When you approach lease discussions with organized financials, you immediately stand out. Clean balance sheets, income statements, and cash flow reports send the message that your company is stable and capable of meeting obligations. This often translates to:

- Lower deposits or security requirements

- Access to longer lease terms

- Greater flexibility in renewal options

- Potentially lower monthly rates

In short, accounting gives you credibility. Landlords want predictable tenants. If your books show consistent growth and controlled expenses, you’re in a strong position to negotiate.

Prepaid Expenses and Why They Matter

One often-overlooked accounting area that can directly affect lease deals is how you handle expenses like insurance, utilities, and rent. These are considered prepaid expense items in accounting. Properly recording them demonstrates that you understand cash flow management. If a landlord sees that you plan ahead and allocate resources responsibly, it reassures them that you won’t miss rent payments when large bills come due.

The Role of Cash Flow in Lease Approvals

Cash flow is king in leasing. Even if your business is profitable on paper, poor cash flow management can signal risk. Accounting ensures you’re tracking:

- When money is coming in (customer payments, sales cycles)

- When money is going out (leases, utilities, payroll)

- How much cushion you maintain month-to-month

Many landlords will review not just your profitability but also whether your cash flow suggests you can weather slower months. With proper accounting, you can present a clear picture that you’re financially resilient.

Benefits of Organized Financial Statements

Landlords and property managers often request financial statements as part of the lease application. Having organized reports ready offers several benefits:

- Professionalism: Shows you treat finances with seriousness.

- Transparency: Reduces back-and-forth during negotiations.

- Efficiency: Speeds up the approval process, which can be crucial in competitive markets.

- Confidence: Positions you as a tenant worth investing in.

These aren’t just “nice-to-haves.” They’re often the deciding factors that determine whether you land the space you want or lose out to another business.

What Landlords Look for in Tenant Financials

From a landlord’s perspective, leasing space is an investment. They want to know that their asset is safe with you as a tenant. Most landlords look for:

- Consistent revenue growth

- Positive cash flow trends

- Controlled operating expenses

- Low debt-to-equity ratios

- Reliable credit history

If your accounting clearly reflects these strengths, you’re not just another applicant—you’re a desirable long-term tenant.

How Accounting Supports Lease Renewals

The role of accounting doesn’t stop after you sign the lease. When renewal time comes around, landlords may reassess your financials to adjust rates or determine whether to extend favorable terms. Businesses that demonstrate steady growth, responsible expense tracking, and healthy margins often secure better renewal terms than those with shaky records. Accounting keeps you prepared not just for the first deal but for every lease cycle.

Mistakes Businesses Make in Lease Accounting

While proper accounting helps, poor practices can harm negotiations. Common mistakes include:

- Mixing personal and business expenses

- Failing to properly record prepaid expenses

- Overlooking hidden lease costs (maintenance, CAM charges)

- Inconsistent or outdated financial statements

- Relying solely on tax filings instead of full reports

These missteps can make landlords question your ability to meet obligations. Fortunately, they’re avoidable with discipline and professional oversight.

Accounting and Long-Term Savings

Securing a lease is about more than signing a contract—it’s about positioning your business for long-term success. Proper accounting helps you avoid unexpected costs, negotiate better terms, and maintain strong landlord relationships. Over time, this can save thousands of dollars in reduced deposits, lower rates, and minimized penalties. Think of accounting as an investment in your business’s real estate strategy.

Final Thoughts

Accounting is often seen as a back-office function, but when it comes to leases, it plays a front-line role. Well-kept books make you more attractive to landlords, give you leverage at the negotiating table, and help you secure terms that truly support your business growth. Whether it’s handling prepaid expense items correctly or simply presenting clear financial statements, proper accounting is one of the most powerful tools businesses can use to land better lease deals.

A strong lease isn’t just about location—it’s about financial credibility. And that starts with accounting done right.

The 5 Best Ways to Find Business Space for Your Service Company

Finding the right business space can make or break your service company’s reputation, operations, and growth potential. Whether you’re in consulting, legal services, marketing, or property maintenance, the space you occupy speaks volumes about your professionalism and credibility. From visibility to logistics, there’s plenty to consider—and plenty of options beyond scrolling endless listings. Here are five powerful ways to land a business space that fits your brand, your budget, and your future.

1. Tap into Local Commercial Brokers

Commercial real estate brokers aren’t just for big companies—they’re goldmines of market intel and off-market opportunities. A broker specializing in your sector can help negotiate better lease terms and steer you away from properties with hidden operational pitfalls.

Why it works:

– Brokers have access to listings not publicly advertised.

– They can assess zoning, accessibility, and proximity to competitors.

– Many offer guidance through lease vs. purchase decisions.

Pro Tip: Look for brokers who’ve worked with similar service-based businesses. They’ll understand your unique flow of clients, hours of operation, and layout requirements.

2. Leverage Online Listing Platforms Strategically

Sites like ROFO offer thousands of searchable commercial properties. But instead of casting a wide net, filter with precision. Use advanced search tools to narrow by square footage, property type (office, flex space, retail), lease length, and amenities.

Optimization tips:

– Set alerts with specific keywords like “service suite,” “turnkey,” or “client-ready.”

– Examine whether properties allow interior customizations or signage.

– Cross-reference listings with local zoning maps and neighborhood reputation.

SEO Angle: Create your own content (like this post!) targeting phrases such as “best office spaces for [your service type] in [your city]” to attract landlords actively searching for tenants.

3. Explore Co-working and Shared Office Providers

For startups and small-scale service companies, shared spaces offer flexibility without long-term commitments. Providers like WeWork, Regus, and local hubs often have private offices, mail services, and client-ready conference rooms.

Ideal for:

– Businesses needing a professional front without full-time overhead.

– Early-stage ventures that want scalable space as they grow.

– Remote-first teams needing occasional in-person meetups.

Bonus: Many co-working spaces foster networking with other business owners, leading to referrals and cross-industry partnerships.

4. Network Within Your Industry and Local Chambers

Word-of-mouth still reigns in business real estate. Attend local chamber of commerce meetings, business expos, or trade associations relevant to your service niche. Building owners and current tenants often share upcoming vacancies before they’re listed publicly.

Why it matters:

– Off-market spaces often come with more negotiation flexibility.

– You’re engaging with landlords who prefer long-term tenants with referrals.

– Chambers often have exclusive access to municipal development plans, including new commercial builds.

Example: A legal tech firm may learn about underutilized floors within law office buildings looking for synergies. Likewise, a digital marketing service might tap into creative hubs looking to fill spots near design studios.

5. Partner with Property Developers and Real Estate Investors

New-build projects and under-renovation properties offer massive customization potential. Developers often seek anchor tenants early on to help shape the layout and amenities. If you have a solid business model and brand, this approach gives you influence over the final design—and potentially discounted rent.

Consider this approach if:

– You need specialized layout features like client lounges, workshop areas, or tech labs.

– You’re expanding regionally and want uniformity across locations.

– You’re willing to wait several months for a space to be ready.

How to connect: Reach out via LinkedIn, local business events, or real estate investment groups. Pitch your company as a stable, service-driven tenant with long-term upside.

Finding business space for a service company isn’t just about square footage—it’s about alignment with your goals, customer experience, and operational needs. By going beyond traditional search methods, you gain access to spaces that reflect the quality of service you provide. Whether you’re booking boardrooms or fielding clients for consultations, the right environment elevates everything.

Want help tailoring your next move to your brand, audience, or location? Let’s brainstorm space search strategies customized for your niche.

DSCR Loans: A Smart Financing Option for Real Estate Investors

What Is a DSCR Loan?

A DSCR loan—short for Debt Service Coverage Ratio loan—is a type of investment property mortgage that qualifies borrowers based on the income generated by the property, rather than the borrower’s personal income. This makes it especially attractive for:

- Real estate investors with multiple properties

- Self-employed individuals or business owners

- Borrowers with complex or inconsistent tax filings

- Foreign nationals investing in U.S. real estate

Rather than reviewing tax returns or W-2s, lenders focus on the property’s cash flow to determine loan eligibility.

How DSCR Loans Work

The Debt Service Coverage Ratio (DSCR) is a simple calculation:

DSCR = Gross Monthly Rent ÷ Monthly Mortgage Payment (PITI)

- A DSCR of 00 means the property’s income exactly covers its expenses.

- Most lenders look for a DSCR of 00 to 1.25 or higher, though some offer more flexible guidelines.

- In some cases, a DSCR below 1.00, or No Ratio, may still qualify with compensating factors, such as a strong credit score or larger down payment.

Benefits of Using a DSCR Loan

1. No Personal Income Verification

Borrowers do not need to provide tax returns, pay stubs, or employment verification—making DSCR loans ideal for investors with write-offs or irregular income.

2. Fast Approvals

With fewer documentation requirements, the underwriting process is generally faster than traditional loans.

3. Scalable for Portfolio Growth

Investors can use DSCR loans to purchase multiple properties, often with more flexible exposure limits than standard Fannie Mae or Freddie Mac guidelines.

4. Ideal for Rental Market

High demand for short-term and long-term rentals in neighborhoods makes DSCR loans well-suited for investment landscape.

DSCR Loan Requirements

While guidelines vary by lender, common requirements include:

- Minimum credit score (typically 660–680 or higher)

- Down payment of 20–25% (some lenders offer lower options)

- Property appraisal with market rent analysis

- DSCR typically ≥ 1.00

- Cash reserves may be required depending on the loan size

Eligible Property Types

DSCR loans can be used to finance:

- Single-family rentals

- Condominiums and townhomes (subject to condo association review)

- 2–4 unit multi-family properties

- Short-term rentals (Airbnb/VRBO) in approved zones

- Mixed-use properties (in some cases)

An Example

Miami’s Real Estate Heatwave: Why DSCR Loans Are Fueling Investor Success

Miami remains a magnet for real estate investors, consistently ranking among the hottest markets in the U.S. Domestic buyers and international investors alike are flocking to the area, drawn by strong rental demand, upward-trending property values, and the city’s reputation as a dynamic economic hub.

For those aiming to grow a portfolio of income-producing properties, the Debt Service Coverage Ratio (DSCR) loan is emerging as a strategic financing option. Unlike traditional mortgages that rely heavily on personal income verification, DSCR loans focus on the cash flow generated by the property itself. This allows investors to qualify based on rental income projections rather than personal earnings, making the process faster, more flexible, and scalable.

Why is this a game-changer for real estate investors? With Miami’s competitive rental market and strong appreciation trends, DSCR financing provides a streamlined path to portfolio growth. Investors can focus on identifying high-yield properties, optimizing returns, and scaling their holdings—all without the typical hurdles tied to personal financial documentation.

Whether you’re acquiring your first investment condo or expanding into multifamily units, DSCR loans in Miami enable a simplified route to building long-term wealth in one of the nation’s most lucrative real estate environments.

Choosing the Right Property Management: A Complete Guide

For a landlord or investor, managing a property single-handedly can be an incredibly difficult job. From the never-ending list of tasks, starting from advertising the unit and screening applicants, performing maintenance, and being aware of the rental laws, there is always something that would need your immediate attention.

Property management companies help solve this problem. In Boston, things can get even more complicated with the city’s unique regulations combined with its ever-active rental market.

Read this guide as we aim to assist you in figuring out the importance of property management, how to make the selection, and the most important steps on why to ask before choosing one.

Why Property Management Is Essential for Landlords

For those who may not know, managing a rental property is no easy feat. From maintenance to ensuring all legal prerequisites are met, a landlord has a lot to keep track of and comply with.

As someone who manages multiple properties or is simply busy, it is all too easy to lose control of day-to-day processes. Good thing for landlords, there is no need to worry since there are companies that specialize in property management.

These companies will ensure that the operations of your rental property business will run smoothly on a day-to-day basis. For example, they will make certain to screen potential tenants while also adhering to the multifaceted rental laws and policies related to Boston.

It is especially common for most landlords to grapple with tenants who tend to pay rent late, struggle with uncooperative tenants, or face legal issues. Let a company take care of these issues so you can focus on other more important matters.

How to Choose the Best Property Management Company

When deciding how to improve the management of your rental property, it’s crucial to choose a property management company that aligns with your goals and expectations. This makes it important to list down your goals alongside the property manager’s past experience and range of services offered in order to come to the right conclusion.

Here’s a closer look at how to choose the best property management company for your asset:

Experience and Reputation

Always ensure a company has a good reputation and solid reviews on property management. Conduct a broad search online to check reviews, ask other landlords, and see if they have handled properties similar to yours in the past.

Having years of experience on the belt of a company is good as they will be able to tackle issues efficiently while still keeping reliability as their top priority. It would also be ideal to see if they focus on the Boston rental market, since having knowledge of the local trends and tenant needs will only make your property more appealing.

Knowledge of Local Laws

Boston has various laws surrounding rentals and leases. When choosing property managers in Boston, it’s important to find someone who understands the local rental market and regulations.

on from expensive disputes while ensuring that your tenants are given the security they need. Ask them how they ensure to remain updated on the Boston laws while being legally focused. This, in return, will allow a more precise decision to be made.

Communication and Transparency

A property manager is expected to focus and prioritize the needs of landlords, tenants, and the rental property. Seek a person with outstanding public relations ethics who is keen on ensuring that you are well updated on the status of your property.

From giving information, updating, sending reports on finances, and handling rent payments from new tenants, their openness builds trust. You will want to steer clear of hidden fees and a lack of honesty.

Range of Services

Factors like rental or marketing strategy might change depending on the property management company. With such variety, it is relevant to understand whether they cover tenant screening, maintenance issues, legal documentation, and marketing activities. Do they help with the collection of rents and emergency repairs?

Ultimately, it is useful for landlords in Boston to understand these factors when picking a property management company to ensure their needs are met excellently.

Choosing the Right Commercial Property for Your Business

As a business owner, you can work from anywhere you’d like. However, if you want your business to grow, separate your business from your home, and employ a large team to help you, you will likely need a commercial office space for convenience. You’ll need to find the perfect space to grow your business, particularly for your industry. You’ll need a location that offers continuous demand from both residential and commercial clients in the long term. If you’re ready to take the plunge and choose the best property for your business, you will want to familiarize yourself with the smartest steps to take and what features to consider first.

Prepare Your Business

Before you choose the location for your business, you’ll want to ensure you’ve adequately prepared and earned qualifications. Many industries require professional licensing, especially if you own a business.

Plumbing